Absolute Return Overlay Solutions: The Best Hope?

Multi-Asset team explains potential benefits of portable alpha overlays, which can meaningfully enhance returns over strategic allocations.

Capturing unfunded alpha opportunities using cash efficient instruments

We believe expected returns on traditional public market investments are likely to be considerably lower over the next 10 years compared to those of the last decade. We think equity returns are likely to be lower given continued expected decline in developed markets’ economic growth, and richer valuations following the strong performance of equity markets relative to underlying earnings. This has not been altered by the impact of COVID-19. In any rational analysis, traditional ways of enhancing those returns are not likely to fill that shortfall. Read our latest Capital Market Assumptions to learn more.

Given this challenging outlook, what can asset owners do to better position their portfolios to meet required rates of return without taking on too much undue risk? Below we review three common approaches to enhancing returns through strategic portfolio allocations and introduce an alternative approach – implementing a portable alpha overlay – that goes beyond the portfolio allocation decision to potentially add meaningful excess returns.

Enhancing the diversification of a portfolio can increase the expected return while decreasing overall risk.

To enhance expected returns over strategic allocations, asset owners have frequently looked to outside asset managers to provide alpha (excess return) above traditional public market passive investments.

Private assets are much less liquid than their public market counterparts, and typically employ leverage to enhance returns.

Investors can capture unfunded alpha opportunities in their portfolio with cash-efficient instruments without distorting their strategic asset allocation.

And How Does it Work?

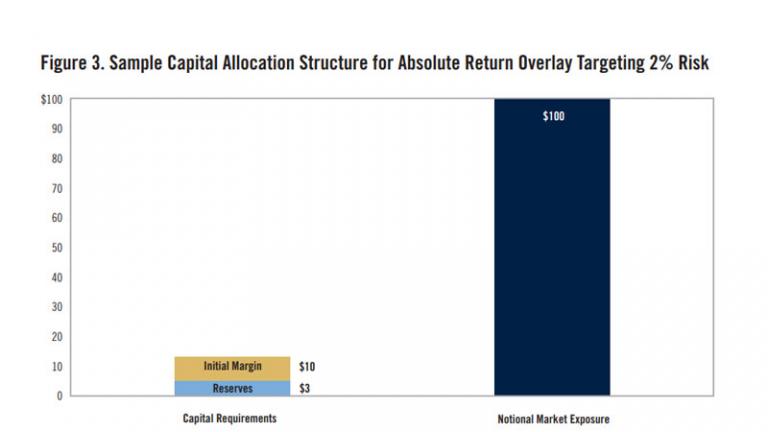

A portable alpha overlay is an uncorrelated and unfunded separate source of excess returns generated by active management. Alpha strategies that use liquid derivative instruments do not have to be fully funded. Consider an absolute return strategy targeting a 0.5 Sharpe ratio implemented through liquid futures and currency forwards. An investor targeting 2% risk can expect about 1% alpha over the strategic allocation. This can be achieved by deploying 100% notional and dedicating only about 13%* of capital to the strategy. The figure below shows a typical breakdown of the collateral requirements for such a strategy. Given our assumptions, the expected return on capital^ is about 8%.

Through a portable alpha overlay, PGIM Quant offers an uncorrelated and partially funded separate source of excess return generated by active management. Investors can capture unfunded alpha opportunities in their portfolio with cash-efficient instruments without distorting their strategic asset allocation.

Utilizes cash allocation from the underlying strategic portfolio.

Customized based on desired target excess return and risk tolerance.

Liquid instruments mean lower cost of implementation, therefore more flexibility to offer better terms to investors.

Excess returns are diversifying to the asset owner’s strategic portfolio.

Risk and drawdown management are critical elements of the investment process.

These strategies seek to capture risk premia and mispricings across asset classes and may provide a good fit for portable alpha overlays. The key features of these strategies include:

There can be no guarantee that this objective will be achieved.

Head of Multi Asset

Marco Aiolfi

Head of Multi-Asset Portfolio Design

Lorne Johnson

Multi-Asset team explains potential benefits of portable alpha overlays, which can meaningfully enhance returns over strategic allocations.

Our holdings-based and factor-mimicking portfolio analyses provide insights into the behavior of carry strategies.

A new approach to explore a link between the well-known macroeconomic exposures of traditional asset classes and those of value premia in a multi-asset context.

* We assume the initial capital commitment is set using a 5% initial margin for 100% notional exposure, and that when market volatility spikes, the initial margin can double. We set aside an amount equivalent to the expected maximum drawdown of the strategy (defined as 1.5 times the target risk) to buffer against margin calls.

^ Return on capital is computed as expected alpha over initial capital commitment. In our example of a strategy targeting 2% risk with expected alpha of 1% (Sharpe ratio of 0.5) and an initial capital commitment of 13%, the expected return on capital is computed as 1%/13%=7.7%.

Diversification does not protect against a loss in a particular market; however, it allows you to spread that risk across various asset classes.

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.